Memory is emerging as the binding constraint in AI infrastructure, and Samsung Electronics’ Q1 2026 results quantify its impact on earnings.

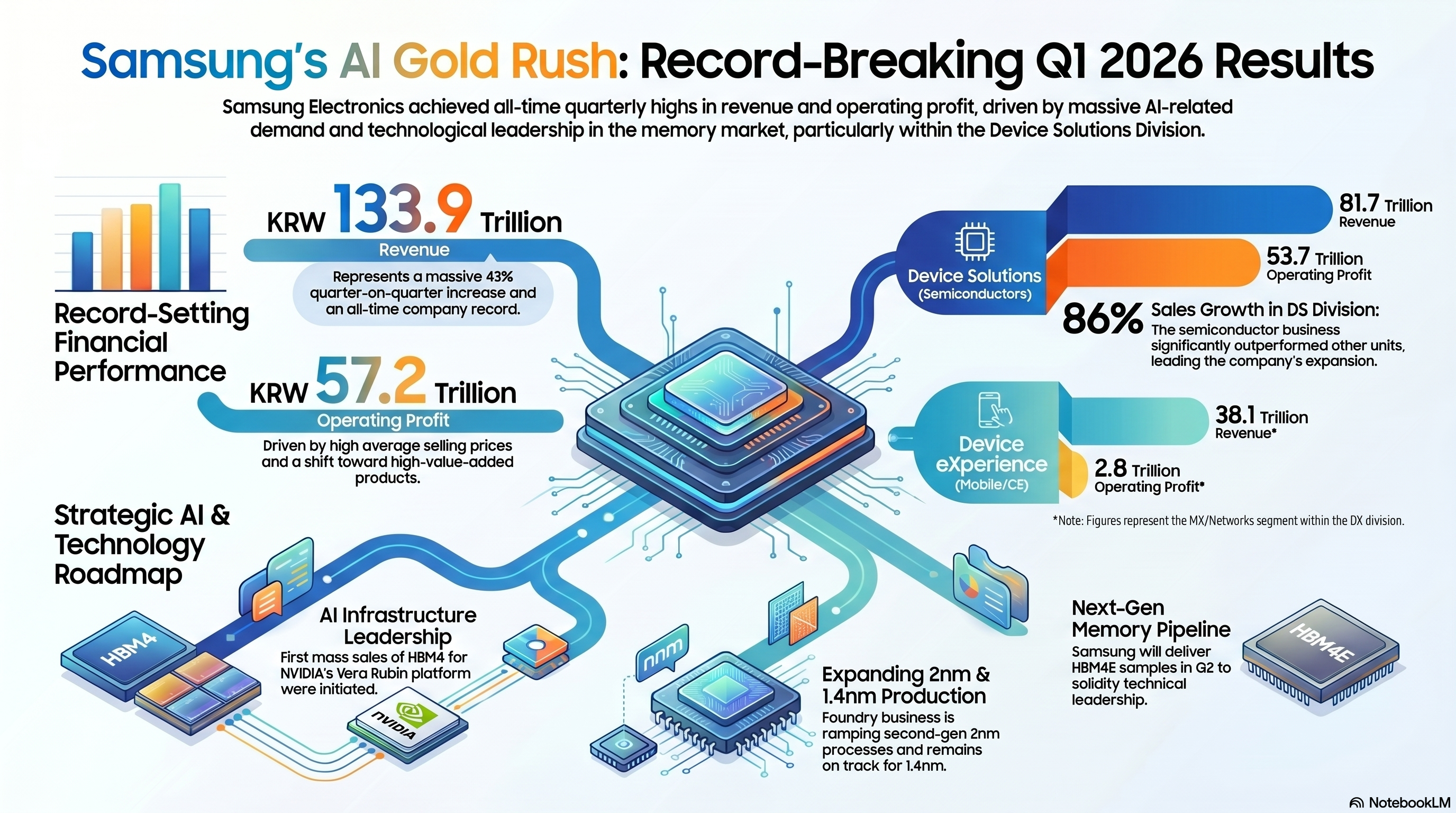

Samsung Electronics reported a record Q1 2026, with ₩133.9T in revenue and ₩57.2T in operating profit, driven overwhelmingly by its semiconductor business. The results underscore a structural shift: memory is now the primary value driver in Samsung’s earnings mix, with DS contributing ~94% of total operating profit.

Why this stands out

Memory is transitioning from cyclical commodity to AI infrastructure bottleneck. Pricing power has shifted to suppliers as hyperscaler AI capex accelerates and supply remains constrained.

What is powering growth

- Memory leadership: The Memory Business delivered record revenue and profit, supported by higher ASPs and strong demand for AI server infrastructure.

- HBM4 ramp: Samsung has begun mass production for Nvidia-linked platforms, with HBM4E sampling planned, positioning it deeper in AI accelerator supply chains. Nvidia remains a key demand anchor.

- Product mix shift: Growth increasingly concentrated in HBM4, DDR5, and enterprise SSDs tied to AI workloads and KV cache demand.

What to watch

- Supply-demand gap: Management flagged that demand continues to exceed supply into 2027, with multi-year binding contracts already signed.

- Competitive dynamics: SK Hynix retains leadership in HBM, keeping execution and yield as key swing factors.

- Downstream pressure: Elevated memory pricing is compressing margins in mobile and display, highlighting portfolio asymmetry.

Big picture

Samsung is benefiting from a structurally tight memory cycle defined by AI infrastructure demand. The upside is clear: sustained pricing power and high utilization. The constraint is equally clear: execution in HBM and managing cyclicality once supply expands.