AMD’s Data Center segment hit $5.8Bn in a single quarter—more than the company generated in total revenue just two years ago. That single fact captures what AMD’s business has become.

What’s Driving Growth

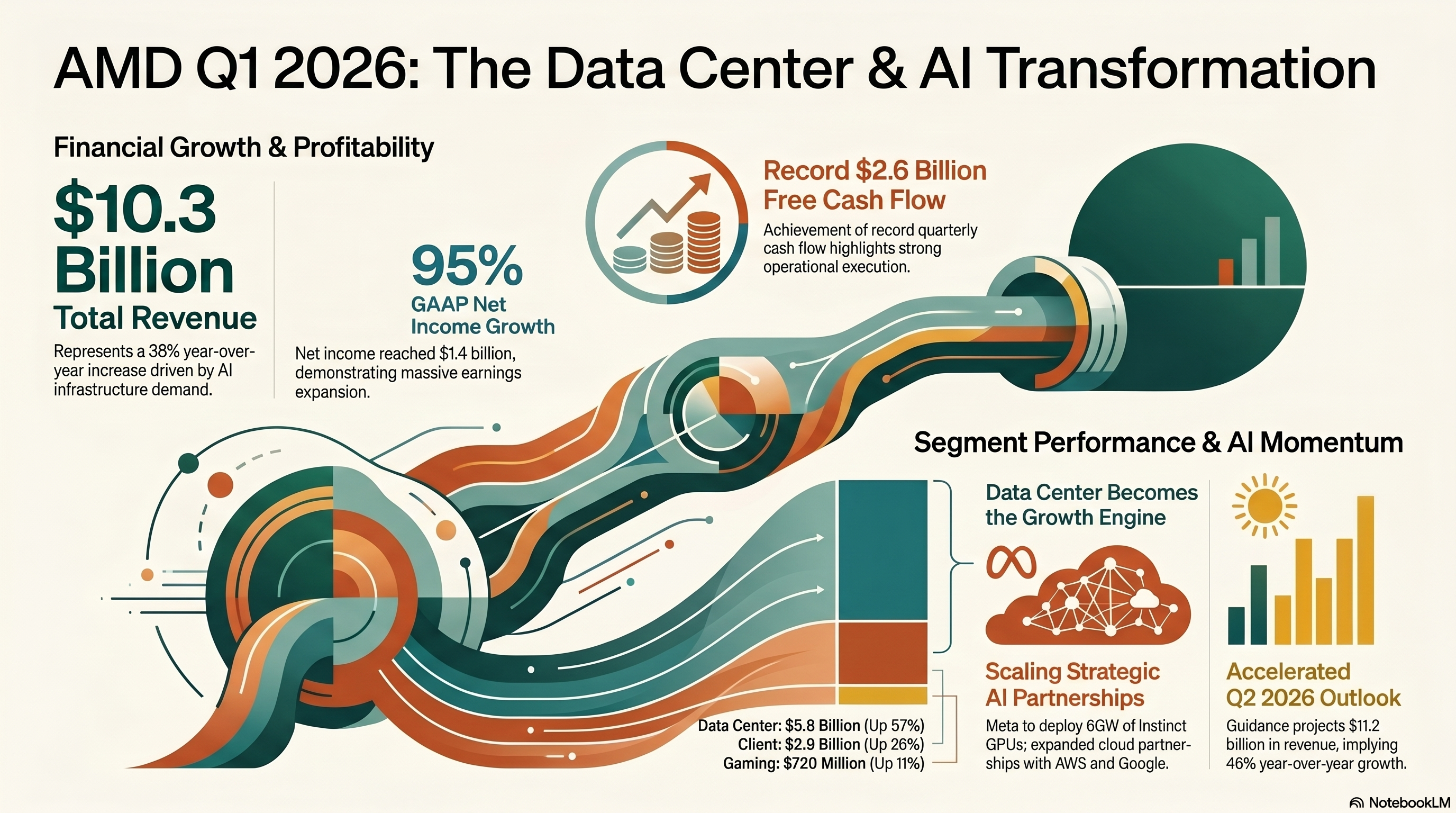

AMD reported $10.3Bn in revenue, up 38% year-over-year and ahead of expectations. Sequentially, revenue was flat—but that masks a clear shift in mix.

Data Center hit a record $5.8Bn, up 57% year-over-year and 7% sequentially, now contributing more than half of total revenue. EPYC CPUs continue to gain server share across cloud and enterprise, while Instinct GPUs are scaling rapidly into AI infrastructure deployments. Client delivered $2.9Bn, up 26% year-over-year, driven by Ryzen momentum across both consumer and commercial segments. Gaming came in at $720Mn, up 11% year-over-year but down 15% sequentially on seasonality. Embedded returned to growth at $873Mn, up 6% year-over-year.

Why It Matters

Data Center is clearly doing the heavy lifting, and the gap versus other segments is widening. The rest of the portfolio, however, is not breaking. Client and Gaming softness is largely seasonal, while Embedded is showing early signs of recovery, with double-digit sequential growth expected in Q2.

The one pressure point is Gaming, where second-half revenue is expected to decline more than 20% versus the first half due to higher memory and component costs. AMD is guiding Q2 revenue to $11.2Bn, implying 46% year-over-year growth and around 9% sequential growth, led by Data Center and Embedded.

The Big Picture

Data Center is now the core engine—but multiple parts of the portfolio are moving in the right direction simultaneously. EPYC and Instinct are scaling together in AI infrastructure, Ryzen is gaining ground in commercial markets, and Embedded is stabilizing after a prolonged downcycle.

Apart from Gaming’s near-term headwind, the numbers point to a business increasingly anchored in durable, large-scale compute demand rather than traditional cycles.